Payment for order flow (PFOF) is the compensation paid by venues like Citadel to brokerage companies like TD Ameritrade in exchange for routing client orders to the venue instead of sending them directly to the stock exchange.

The first 606 disclosures with venue details were officially published for the first quarter of 2020. Our current database includes 251,373 data points and covers all data from January 2020 to December 2022.

Brokers are required to publish their statements by the end of January, April, July, and October for the previous quarter. The statistics, comparisons and charts in this article are updated annually or upon media request.

If you use the data provided as a source for your story, please cite https://daytradingz.com/payment-for-order-flow/ as a reference.

| Payment for Order Flow | Detail |

|---|---|

| Required by | U.S. Securities and Exchange Commission |

| SEC Rule | 606 |

| Release Dates | Apr. 30, Jul. 31, Oct. 31, Jan. 31 |

| Paid by | Venues |

| Received by | Brokers |

| Acronym | PFOF |

Statistics

In 2020, $2.75 billion were paid to the 10 leading retail brokerages TD Ameritrade, Robinhood, E*Trade, Charles Schwab, Fidelity, Webull, TradeStation, Ally Invest, Bank of America and Wells Fargo. TD Ameritrade and Robinhood made the most money by selling order flow to venues like Citadel Securities, Global Execution Brokers, and Virtu Americas.

The released data of 2021 revealed that the payment for order flow grew by 32% to $3.62 billion in 2021 (vs $2.75 billion on 2020). TD Ameritrade further extended its market leadership in this segment to over 1 billion (+24%), while Webull saw the biggest percentage gain (226%).

The PFOF statistics of 2022 indicate a decline in the overall payment for order flow back to the 2020 level. The overall PFOF paid to the 10 leading U.S. brokerages in 2022 is $2.89 billion, compared to $3.62 billion in 2021 and $2.75 billion in 2020. Robinhood lost about $99.2 million and E*Trade $29.6 million in 2022 vs. 2020. In contrast, Webull earned $185.1 million and Charles Schwab $73.1 million more.

| Brokerage | 2020 (in $) | 2021 (in $) | 2022 (in $) |

|---|---|---|---|

| TD Ameritrade | 1,148,550,502 | 1,421,044,615 | 1,171,642,061 |

| Robinhood | 687,094,992 | 974,166,848 | 587,901,295 |

| E*Trade | 402,493,959 | 454,431,992 | 372,848,438 |

| Charles Schwab | 245,463,984 | 319,998,932 | 318,590,047 |

| Webull | 63,853,903 | 208,448,408 | 248,959,874 |

| Fidelity | 134,314,911 | 161,850,777 | 121,835,081 |

| TradeStation | 41,844,854 | 58,203,831 | 54,671,224 |

| Ally Invest | 15,270,053 | 13,762,279 | 9,652,332 |

| Wells Fargo | 5,159,316 | 6,107,099 | 3,320,686 |

| Bank of America | 8,640,784 | 3,328,754 | (2,099,125) |

| Grand Total | 2,752,687,260 | 3,621,343,534 | $2,887,321,913 |

Quarterly Statistics

The payment for order flow income consolidates on a mid level. The fourth quarter of 2022 generated a total of $665,902,306 of income for the top 10 brokerage firms. This is the second-lowest quarter since the beginning of payment for order flow tracking, and 13.2% below average.

The detailed quarterly split per broker provides further insights into the quarterly results.

The split per broker shows that the PFOF income declines across the board, while we can see that Bank of America does not make money with PFOF anymore.

TD Ameritrade still dominates the payment for order flow business, followed by Robinhood and E*Trade.

Broker Statistics

1. TD Ameritrade Payment for Order Flow

The annual TD Ameritrade payment for order flow income in 2020 was $1.15 billion, with a monthly average of $96 million. TD Ameritrade continues to have the highest revenue among all brokers in this list. The monthly average 1-12/2021 grew to $118 million for a grand total of $1.42 billion. In 2022, the monthly average was $97.6 million, and $1.17 billion in total.

2. Robinhood Payment for Order Flow

The Robinhood payment for order flow saw significant growth in 2020 to $0.69 billion with a monthly average of $57 million. The trading app is more popular than ever before. New mobile trading apps like Webull may take some market share (Webull review), but Robinhood leads the segment of mobile trading apps (Robinhood review). The monthly average 1-12/2021 grew to $81 million for a grand total of $0.97 billion PFOF. In 2022, the monthly average was $48.99 million, and $587.9 million in total.

3. E*Trade Payment for Order Flow

The E*Trade payment for order flow is the third-largest in the list, with a total of $0.40 billion in 2020 and a monthly average of $34 million. The monthly average 1-12/2021 grew to $38 million for a grand total of $0.45 billion PFOF. In 2022, the monthly average was $31.1 million, and $372.8 million in total.

4. Charles Schwab Payment for Order Flow

The Charles Schwab payment for order flow is the 4th-largest in the list, with a total of $0.25 billion in 2020 with a monthly average of $20 million. The monthly average 1-12/2021 grew to $27 million for a grand total of $0.32 billion PFOF. In 2022, the monthly average was $26.5 million, and $318.6 million in total.

Charles Schwab acquired TD Ameritrade and concluded the acquisition for $22 billion. The deal was announced in November 2019 and completed in October 2020. Therefore, TD Ameritrade and Charles Schwab payments for order flow go to the balance sheets of Charles Schwab (SCHW).

5. Webull Payment for Order Flow

The Webull payment for order flow is low compared to the competitors, but it shows the strongest percentage gains compared to the previous year. The PFOF 1-12/2021 is 226% higher vs. 1-12/2020. June 2021 was also the strongest PFOF month in the history of Webull, with a total of $20 million received. In 2022, the monthly average was $20.7 million, and $249.0 million in total. With this steady growth, it is most likely that they will outrank other brokers in the mid-term.

6. Fidelity Payment for Order Flow

Fidelity belongs to the top 5 brokerages receiving the highest PFOF compensation from venues. The PFOF income in 2020 was $134 million with a monthly average of $11.2 million. In 1-12/2021, the monthly average increased to $13.5 million and a total of $162 million in 2021. In 2022, the monthly average was $10.2 million, and $121.8 million in total.

7. TradeStation Payment for Order Flow

In 2020, TradeStation received $41.8 mn PFOF with a monthly average of $3.5 mn. The payment for order flow income 1-12/2021 grew significantly by +39% compared to 1-12/2020. In 2022, the monthly average was $4.6 million, and $54.7 million in total.

8. Ally Invest Payment for Order Flow

Ally Invest is the 3rd-smallest brokerage company on the list and received only $15.3 mn PFOF from venues in 2020, and $13.8 mn in 2021. In 2022, the monthly average was $0.8 million, and $9.7 million in total.

9. Wells Fargo Payment for Order Flow

Wells Fargo received $5.2 mn PFOF from venues in 2020, and $6.1 mn in 2021. In 2022, the monthly average was $0.3 million, and $3.3 million in total.

10. Bank of America Payment for Order Flow

It seems that Bank of America now pays more money for order flow to stock exchanges than they receive from venues for routing order flow to them. The cause for this could be a strategic change for order routing principles or the higher demand from Bank of America clients to route the orders directly to a specific stock exchange instead of using smart routing.

Venue Statistics

The venues are those who pay the brokerage houses for their order flow. Looking at the per venue statistics paints a clear picture of the market leaders. Citadel, Global Execution Brokers and Dash Financial Technologies dominate from the venue side with about about 62% of the overall business.

| Venue | 2020 (in $) | 2021 (in $) | 2022 (in $) |

|---|---|---|---|

| Citadel | 1,122,990,199 | 1,423,975,903 | 995,497,864 |

| Global Execution Brokers | 447,128,821 | 640,126,586 | 428,812,027 |

| Dash Financial Technologies | 111,849,476 | 204,153,712 | 362,604,118 |

| Wolverine | 199,868,910 | 418,246,526 | 323,973,374 |

| other | 243,999,928 | 237,609,202 | 302,673,515 |

| Virtu Americas | 311,970,264 | 329,811,280 | 236,920,852 |

| G1 Execution Services | 195,365,545 | 147,008,781 | 138,106,736 |

| Two Sigma Securities | 63,545,982 | 140,906,710 | 70,223,117 |

| UBS Securities | 55,968,134 | 79,504,834 | 28,510,311 |

| Grand Total | 2,752,687,260 | 3,621,343,534 | 2,887,321,913 |

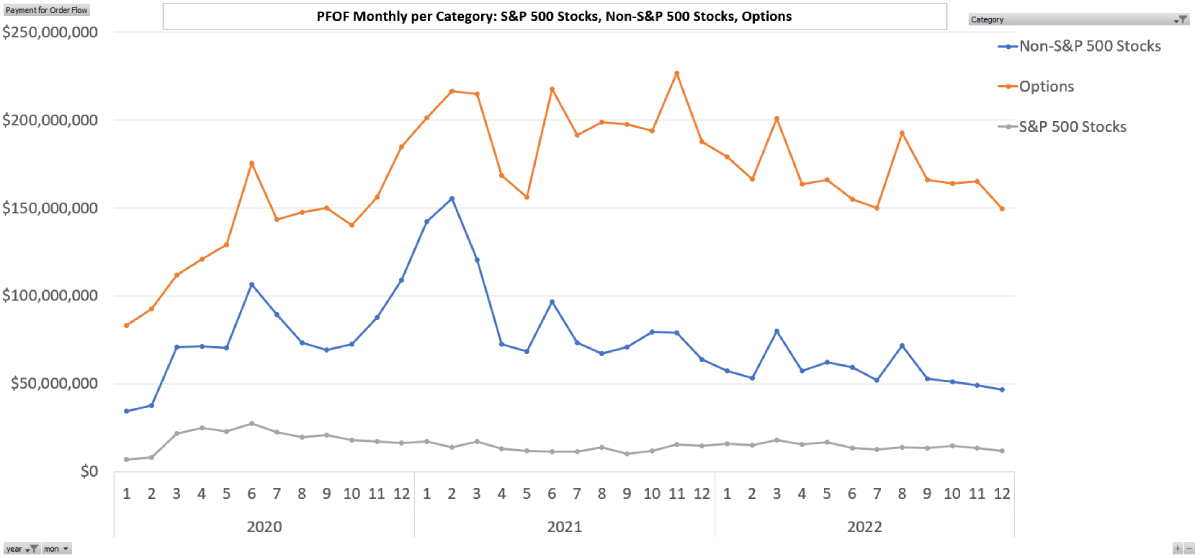

Payment for Order Flow by Asset Category

The categories Options and NON-S&P500 stocks dominate the payment for order flow revenues. It is not a surprise since the spread, which is the baseline for the income, for S&P500 stocks is small since the liquidity is immense. Therefore it is hard to generate price improvements for clients or meaningful income to be shared between venues and brokers. The payment for order flow is dominated by the options trading category.

You can also see that various venues are specialized in one or the other asset category. Venues like Citadel pay for order flow in all three categories, from S&P 500 stocks to NON-S&P 500 stocks and options. Global Execution Brokers and Dash Financial Technologies are specialized in options, while Virtu Americas focuses on stocks.

Payment for Order Flow by Month

In 2020, we saw significant growth in order flow payments, mainly affected by the global challenges. With more people working from home, and higher demand to make money trading the stock market because of zero interests, the online trading industry saw news highs quarter by quarter.

Another reason for the growth was the introduction of zero commission offerings across all leading online brokerages. That’s an interesting situation. Zero commissions boost payment for order flow revenues since retail investors trade more because it is free to trade.

In January 2020, the payment for order flow was $124.6 million. In June 2020, we saw a temporary peak at $309.5 million. 2020 ended with a record breaking payment for order flow of $310.0 million in December.

In 2021 we saw the highest payment for order flow month in February, with $385.6 million paid by venues to the 10 leading online brokerages. The strong uptrend was mainly caused by the meme stock fancy initiated by the WallStreetBets Reddit forum. The demand in trading stocks like GME, AMC and BBBY decreased, but the overall trading activity is still on a high level.

In 2022, we had two peaks, one in March and one in August, but other than that, the monthly PFOF was relatively flat from an overall perspective.

Brokerage Mapping

Some brokerages used different company descriptions within the brokerage 606 disclosures, and some also have different company divisions where the payments for order flow are allocated. Here is our brokerage mapping:

Venue Mapping

The list of venues is long, and in some cases, they are also differently mentioned within the brokerage 606 disclosures. Therefore, we mapped the venues and focused on the key players. Here is our venue mapping:

Payment for Order Flow Concept

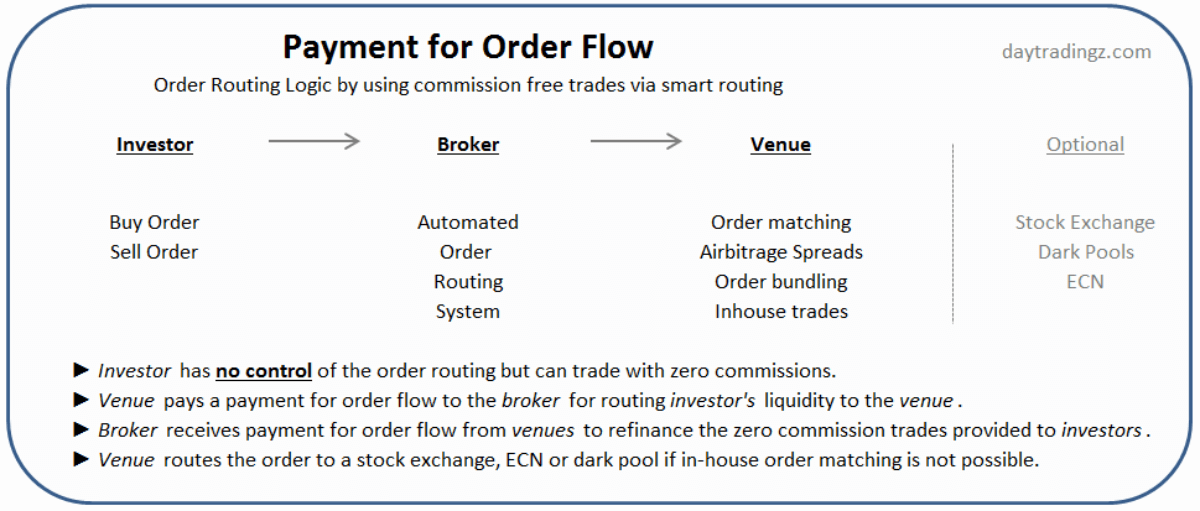

You may ask yourself why a venue does pay money to the brokerage firm if the venue does all the work. The answer lies between the bid and ask; the so-called bid ask spread.

Let’s say you are interested in buying stock of company XYZ. The order book shows a national best bid of $105.50, and the best ask is $106.00. If you send a market order to buy 100 shares for the best possible price, your order would probably be executed at $106.00 (I want to keep this example simple, and things like hidden orders, market depth etc., are left aside.)

If in the next moment the best bid and ask are still at $105.50 and $106.00, and you hit the sell market button to close your position immediately, then your order would probably be executed at $105.50.

In that case, you lost 50 cents per share, which equals a total loss of $50.

If you allow your broker to take care of the order routing, they route the retail order to third party firms like Citadel Securities or Two Sigma Securities, called venues.

They receive thousands of buy and sell orders for hundreds of stock symbols every minute. An algorithm matches the client orders if possible. Since not all orders with exact the same order size arrive at the venue’s system at the exact same time, proprietary algorithms average down the order flow and evaluate the potential of price improvements. The venue always has the option to route the order further to the stock exchange.

Back to our example, your buy market order for 100 shares of company XYZ arrives 10 milliseconds before another trader wants to sell 100 shares of company XYZ by using a market order. Typically you would get filled at the next best ask at $106, and he at the next best bid at $105.5. But the venue now maps both orders using their algorithms and shares the profit made.

A significant portion of the benefit of $0.50 per share goes to the retail traders by providing them with a price improvement. Let’s say the buyer gets a fill at $105.8 instead of $106.00, and the seller receives a fill at $105.7 instead of $105.5. Both traders are happy, they did not pay commissions, and both got a price improvement of 20 cents.

The remaining 10 cents (the difference between $105.7 and $105.8) is the profit for the venue. But the venue shares this profit with the brokerage business, so they pay for order flow. This profit split is the Payment for Order Flow, where the venue pays the retail brokerage firms for sending liquidity to them, based on the order flow arrangements and conditions.

Now you may legitimately ask yourself how a venue or broker could make money if the most significant portion of the benefit goes to the investor via price-improvements. Until the end of 2019, you could only guess how much money was made via payments for order flow.

In the past 6 months, 32,600 people ask search engines every month “How Does Robinhood Make Money.” Thanks to the SEC’s revised requirements in SEC Rule 606, U.S. brokerages must list the exact paments received within the 606 disclosure every quarter since 2020. Now we can answer the question of how much money do retail brokerages make by selling order flow.

Zero Commissions via Payment for Order Flow vs Direct Access Broker Order Routing

Market Potential

January 2021 was a month that we would remember for a long time. Robinhood, Wallstreetbets, Hedge Funds, Citron Research, GameStop, AMC Entertainment, Nokia, BlackBerry dominated the street news.

The Reddit forum r/wallstreetbets grew from 1.8 million members on January 1, 2021, to 7.6 million on January 31, and 10.0 million in April 2021. From April to July 2021, the forum member count grew to 10.7mn, but only by 300,000 more until October 2021. The Robinhood app downloads skyrocketed to new highs, some of the mentioned company stocks explode with temporary gains of over +1,000% and fell 90% after that.

One could only guess how this media presence would affect the payment for order flow revenue.

A controversial discussion already began if payment for order flow is beneficial, transparent, and fair. We may see some regulatory changes in the future.

If brokers are not allowed to receive payments for order flow anymore, a major source of income for them will disappear. Then, the chances are that commissions per trade have to be re-introduced.

Official statistics clearly show that most client orders see price improvements if the orders are routed to the venues. Therefore there is no clear right or wrong.

Direct Market Access vs Payments for Order Flow

Specialized brokers with direct market access don’t rely on payments for order flow. Instead, they charge low fees and enable traders to route their orders to the preferred stock exchange or ECN. Due to the direct order routing, order execution can be beneficial, especially when trading high volumes.

Bottom Line

Selling order flow has become one of the primary sources of income for U.S. Brokers. TD Ameritrade and Robinhood dominate the market, while Webull shows the most significant percentage growth.

Charles Schwab bought TD Ameritrade for $26 billion, and Morgan Stanley acquired E*Trade for $13 billion. We may also see further consolidation activities in the brokerage sector. Depending on how the mergers are executed and which entities remain, the market share per brokerage may change 2021 and beyond.

Payment for order flow became the primary source of income for Robinhood. In 2020, Robinhood had a total net revenue of $958.8 mn and thereof, $687.09 was received via payments for order flow. That means that 71% of total revenues came from PFOF.

Robinhood is listed on Nasdaq with the ticker symbol HOOD since July 29, 2021. The Robinhood stock price will primarily depend on the further development of PFOF income, while other brokers like TD Ameritrade and Charles Schwab have other primary sources of revenue.

The quarterly 606 disclosures are the first step in the right direction. The current media presence shows that even more transparency would be beneficial to the industry.

Investors involved in day trading should keep in mind that zero commissions brokers limit the order routing flexibility. At the same time, direct access brokers allow day traders to choose the order routing ECN and exchange directly.

See Also:

Frequently Asked Questions

What is payment for order flow?

Payment for order flow (PFOF) is compensation paid by trading venues, such as Citadel Securities, to brokerage firms in exchange for routing client buy and sell orders to the venue instead of sending them directly to a stock exchange. The venue profits from the bid-ask spread when it matches orders internally and shares part of that profit with the broker. It is the main reason most US retail brokers can offer zero-commission trading.

Is payment for order flow bad for traders?

It cuts both ways. The clear benefit is zero commissions and frequent price improvement, since orders matched inside a venue often fill better than the national best bid and offer; one broker reported 96.9% of orders improved in a sample quarter. The criticism is that it can compromise routing flexibility and execution quality compared with sending an order to a chosen venue. Official data shows most retail orders do receive price improvement, so there is no clean right or wrong.

How much money do brokers make from payment for order flow?

Based on SEC Rule 606 disclosures, the 10 leading US retail brokerages received about $2.75 billion in 2020, $3.62 billion in 2021, and $2.89 billion in 2022. TD Ameritrade and Robinhood have led the segment, while Citadel dominates the venue side. Options and non-S&P-500 stocks generate the bulk of the revenue, because their wider spreads leave more room for price improvement and profit.

How do I know if my broker uses payment for order flow?

Every US broker must publish a public Rule 606 order-routing report each quarter, which discloses the payments received; searching the broker’s name plus “606 disclosure” is the fastest way to find it. As a rule of thumb, if a trader controls the order routing directly, the broker likely does not receive PFOF, whereas smart or automated routing usually means orders go to venues that pay for them. Direct-access brokers generally do not rely on PFOF.